Published on: January 9, 2023

They can now strive to provide a non-financial experience to customers. This growth has been enabled thanks to the digitization of commerce and fintech infrastructure. The new face of finance gives various players the opportunity to re-position themselves in a value chain to become more industry-agnostic and brand-dependent. Let’s take a look.

Embedded finance has rapidly evolved into an industry disruptor in numerous sectors and gained popularity worldwide - putting intense pressure on many industries to provide a frictionless customer experience. This new face of banking brings together a variety of actors in both unique and revolutionary ways.

It is predicted that in the next ten years, embedded finance will be valued at more than $7 trillion - making it worth double the combined value of the world’s top 30 banks today. [1]

In the embedded finance market, there are three highly developed areas. They are listed as embedded payments, embedded lending, and embedded insurance.

One of the biggest challenges embedded finance providers face is customer experience optimization. Distributors try to create a so called "frictionless" customer journey to avoid the risk of abandonment. When purchasing your shopping cart, you expect multiple payment options, and the execution of them should feel effortless; your card details are automatically entered, or you choose to pay later with the click of a button.

MoneyLive states that 60% of customers expect the option to switch channels during the application process without having to start again, making correct channel integration essential to lower abandonment rates. [3]

Abandonment rates are a key metric for embedded finance providers and their partners. The metric gives an insight into how much friction the end customer experiences. When an end customer encounters friction, the abandonment rate will be higher.

Consumer trust is essential when dealing with financial services. Building trust with the customer using communication is crucial and requires a complete understanding of the customer's expectations. Where a completely frictionless experience seems the top priority, finding a balance in the level of friction you offer is more important. Customers need to experience security because they find comfort in seeing the "payment authorization" screen. This creates a sense of trust. Short and direct communication interactions will be the way forward for embedded lenders supplying smaller transactions.

Lenders must enhance identification and authentication by utilizing mobile authentication and behavioral biometrics to secure the client journey without compromising convenience. However, this needs to be matched by a greater focus on consumer transparency, with lenders investing in cutting-edge analytics and AI to make sure their customer communications are transparent, personalized in the proper language and brand, and comply with legal requirements.

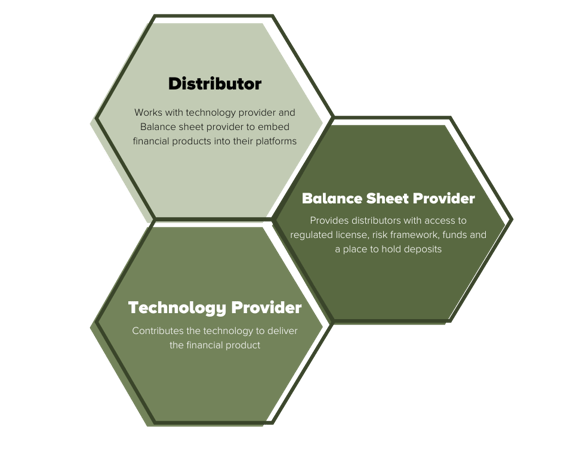

Two kinds of providers are necessary to enable the offering of embedded financial products in their platform. Not all the players benefit equally from the rise of embedded finance. As is common in banking, the revenue is allocated to the risk takers (balance sheet provider) and the distributor that owns the platform.

The application of embedded finance is expected to increase in parallel with the advance of global ecommerce markets. The market growth will push traditional banks to create stronger partnerships with emerging fintech players, providing full embedded finance applications to their customers.

References: